How to Cite | Publication History | PlumX Article Matrix

Arsen Azidovich Tatuev1, Elena Vyacheslavovna Lyapuntsova2, Askerbiy Arsenovich Tatuev3, Violetta Valerievna Rokotyanskaya2 and Zalina Nurmuhamedovna Zhankazieva1

1Kabardino -Balkarian State University named after Kh.M. Berbekov 360004, Kabardino-Balkarian Republic, Nalchik, Chernyshevskogo st., 173 2Moscow State University of Food Production125080, Moscow, Volokolamskoye sh., 11 3North-Caucasian Federal University355035 Stavropol region, Stavropol, Lenin’s st., 133b

ABSTRACT: In the article the advantages of program budgeting in comparison with the traditional one are dealt with the analysis of state programs of the Russian Federation from the point of view of basic elements of efficiency is carried out, the main problems arising in the course of their development are revealed and measures for their further improvement are suggested.

KEYWORDS: budget planning; program budgeting; budgetary policy; efficiency; state programs; budget

Download this article as:| Copy the following to cite this article: Tatuev A. A, Lyapuntsova E. V, Tatuev A. A, Rokotyanskaya V. V, Zhankazieva Z. N. Program Budgeting as a Tool of Introducing a Higher-Level Performance of the Public Sector of the Economy. Biosci Biotech Res Asia 2015;12(2) |

Introduction

Importance

Consecutive introduction of program budgeting in the budgetary process assumes the change of the state policy and can become the main means of modernization of public administration sector. Application of the program format allows making the formation of the budget strategic both financially reasonable and also considering various options of realization of state programs which need further improvement, regarding the formulation of the purposes, use of indicators of an assessment of social and economic efficiency.

Methods

In the real work on the basis of functional and dynamic approach the most important directions of state programs efficiency increase which will allow turning them into the effective instrument of realization of social and economic policy of the state are defined.

Discussion

Introducing program budgeting is an uneasy process, that presumes, among other things, a reform in the system of government management. The transition to program budgeting requires a number of essential changes in the financial activity of the government:

- revising and reforming the financial processes;

- reorganizing management agencies;

- achieving more professionalism in financial activity;

- new proficiencies of the specialists in the public sphere.

From this point of view, program budgeting can be seen as a set of operations, aimed at improving the efficiency and effectiveness of the public sector’s performance. According to many researches, the introduction of program budgeting allows:

а) obtaining the maximum result (output) from the use of limited financial resources;

b) evaluating more objectively, on the basis of the results obtained and costs entailed, the results of the activity of ministries and agencies, performing their functions or delivering services within the limits of their authorities.

In this regard, we can say that program budgeting is based on directly associating the budget expenditures (the use of the financial resources) and the amount and the quality of the provided governmental services (i.e. the outcomes of the performance of ministries and agencies) (Anderson & Anderson & Velandia-Rubiano, 2010; Barro, 1989; Checherita & Rother, 2010). The idea of introducing program budgeting is based on the advantage of increasing the social and economical efficiency and effectiveness of budget expenditures.

Unlike the traditional form of allocating (line-item) budgeting, program budgeting offers a number of advantages, which allows:

- focusing budget expenditures on politically determined and strategically important objectives for social and economical development of the country;

- achieving a direct relationship between the short-term and the long-term forms of budget planning and forecast;

- providing exact agreement between the strategic government’s plans and the budget;

- achieving higher-level accountability of ministries and agencies in the public sector for the targeted and effective use of the granted funds;

- redistributing resources within the framework of implementing particular programs, as well as in favour of more productive and/or priority areas (operations);

- carrying out objective evaluation of the efficiency and effectiveness of budget expenditures on the basis of certain;

- simplifying the structure of the budget;

- achieving higher transparency of the budget information and make it more accessible, for not only the participants of the budget process, but also for the community/society as a whole.

To make these advantages come true, it is vital that the transition to program budgeting should be thoroughly prepared and steadily implemented, be politically sponsored and strictly controlled. Moreover, the consistent implementation of program budgeting in the budgeting process presumes a change in the governmental policy and might become the basic tool of reforming the sector of public administration (Shush & Afanasiev, 2014; Shush and Borodin and Tatuev, 2014; Shush & Borodin, 2014).

To obtain more effect from the implementation of program budgeting, it should be combined with reforms in the sphere of public administration and public finance management.

The program budget differs from the traditional one in that point, that all, or nearly all, costs are allocated to programs, each of them being directly associated with a concrete result (a strategic outcome) of a ministry’s operations, and demonstrates a positive change in the sphere of an agency’s influence. In this respect, a program budget is an opposite to a traditional one, as it is based on the indicators of the result (immediate and ultimate), not on the input of the resources.

Applying the program format allows making the formation of the budget strategically and financially justified, and also, to consider different variants of realization of the programs. However, in practice, it is rarely possible to achieve an optimal combination of both the strategic planning and the budget reasonability (Cochrane, 2011; Gale & Orszag, 2003; Groneck, 2010; Elmendorf and Mankiw, 1999; Hanson, 2007).

The specifics of the federal budget in the Russian Federation are the following, since 2011 its program part has been represented by a set of state programs, whose development can be viewed as an attempt to unite all instruments for achieving the goals of the government’s policy. Today, in the Russian Federation, there are a lot of high-level governmental tasks, that can be solved only if a number of ministries participate. Such tasks are essentially complex trends in the state’s policy, namely, being realized as the governmental programs of the Russian Federation.

At present, 42 programs have been adopted in the Russian Federation, which constitute 5 core building blocks, they are the following: the new quality of life, the innovative development and modernization of the economy, the provision of the national security, the proportional regional development, the effective state. Still the quantity of the governmental programs being implemented and the amount of their financing are being corrected for each subsequent budget cycle (Table1).

Table 1: The distribution of the budget resources among the core building blocks of the government’s programs in the (billion roubles)*

| The quantity of the government’s programs, by blocks | The amount of financing, billion roubles | |||||||

| 2011-2013 yrs | 2012-2014 yrs | 2013-2015 yrs | 2014-2016 yrs | 2011-2013 yrs | 2012-2014 yrs | 2013-2015 yrs | 2014-2016 yrs | |

| The innovative development and modernization of the economy | 17 | 17 | 17 | 17 | 4710.7 | 5982.7 | 5594.3 | 6210.7 |

| The new quality of life | 11 | 13 | 12 | 12 | 14495.5 | 18500.8 | 9749.3 | 10279.0 |

| The effective state | 5 | 5 | 5 | 4 | 4890.3 | 4412.7 | 3378.5 | 3549.2 |

| The proportional regional development | 4 | 4 | 5 | 5 | 782.5 | 1890.3 | 2008.7 | 2262.6 |

| The provision of the national security | 2 | 2 | 1 | 1 | 2513.2 | 7660.8 | 22.4 | 5.3 |

| The expenditures on the realization of the GP operations of the RF, that are regarded as a government’s secret | 2854.9 | |||||||

| TOTAL: | 39 | 41 | 40 | 39 | 27392.2 | 38447.2 | 20753.1 | 25162.2 |

*The source: the official site of the Ministry of Finance of the RF www.minfin.ru

Table 2: The distribution of the budget expenditures by the core blocks of the government’s programs in the years 2011-2016 (billion roubles)*

| The expenditures of the federal budget of the RF | 2011-2013 yrs | 2012-2014yrs | 2013-2015yrs | 2014-2016 yrs | ||||

| % | % | % | % | |||||

| program | 27392.2 | 80.4 | 38447.2 | 93.8 | 20753.1 | 48.1 | 25161.7 | 56.5 |

| non-program | 6679.9 | 19.6 | 2522.7 | 6.2 | 22467.5 | 51.9 | 19348.0 | 43.5 |

| total | 34072.1 | 40969.9 | 43220.6 | 44510.2 | ||||

*The source: the official site of the Ministry of Finance of the Russian Federation, www.minfin.ru

As can be seen from the data in Table 2, since 2013, a reduction has been taking place in the program part of the federal budget expenditures, due to the reduction the number of the governmental programs. In particular, this affected the programs that are heavily financed including the program on the development of the pension system. Thus, the share of non-program expenditures has increased dramatically, since the budgetary appropriations, allocated for the development of the pension system, were planned in the amount of 9320.1 billion roubles.

Despite the fact that in the end of April 2013 the State Duma adopted amendments to the Budget Code of the RF (No. 104-FL dated 7/05/13), that are necessary for the transition to a normal program budget, and these legislative changes should have created an incentive to the formation of the federal budget of Russia in the next budget cycle of the years 2014-2016 in the entirely program format, it did not happen. In addition, the share of program costs of the federal budget in 2014-2016 amounted to 56.5%. It has to do with the circumstance that in the previous year, 2 governmental programs were not approved (39 out of 42 state programs from the index were approved): one – in the sphere of the national defense, another – aimed at the development of the pension system. In connection with that, the expenditures still remained in the non-program part of the budget expenditures. It should be noted, that in 2014-2016 it was planned to direct 8141.7 billion roubles to guarantee the development of the pension system, and 8925.3 billion roubles at hidden costs, including the provision of the national defense.

Additionally, due to the new challenges that the deterioration of the world situation poses, and that limit the domestic possibilities for economical growth, causing a decline in industrial production, the current budget has been seriously modified (Shush & Afanasiev, 2014), as the project of the federal budget for the years 2014-2016 was formed under the conditions of a decrease in the formerly predicted incomes. It is not incidental, that the idea of cutting the state’s expenditures became the main idea of the Budget Message from the President in the year 2013. Sequestration has touched upon most areas of the budget expenditures. The most unlucky turned out to be the housing sector, its expenditures were to be cut in the year 2014 by approximately a quarter (37 billion roubles). The expenditures on education were also cut by 13% (which makes 88 billion roubles).

In this regard it should be noted, that due to the complexity of the macroeconomic situation a project was developed for optimizing the government’s expenditures, which were planned to be reduced by approximately 1.1 trillion roubles; it would mean, among other things, a change in the order of funding the pension system and in reforming the sector of public administration. It comes naturally, that all this, along with pessimistic expectations concerning the profitable part of the budget, could have had only a negative effect on the amounts of financing and on the distribution of the resources from the budget that are going into the implemented government’s programs. However, it is not under-financing that is the primary cause of their low effectiveness, there remains a number of complex problems and issues, that need a serious study.

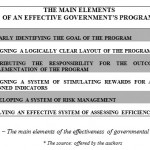

The basic techniques of program budgeting are mostly analogous to the approaches employed in the private sector (stating the mission and strategies, budgeting from zero, budgeting by the accrue method, the use of indicators for assessing the social and economic efficiency, developing a system of risk management, taking risks into account and others), which can be viewed as the main elements of the efficiency and effectiveness of governmental programs.

|

Figure 1: The main elements of the effectiveness of governmental programs * * The source: offered by the authors |

Our analysis gives grounds to say that in most cases the governmental programs need further improvement, for instance, in the part of identifying the objectives. As an example, we could point at governmental program 05 “The provision of quality and affordable housing and related services to the citizens of the Russian Federation”, both objectives of which do not mirror the requirements of actual guidelines – that is, “To make housing more affordable and to improve the quality of housing provision to the population” and “To achieve a higher quality and reliability of the provision of the housing services to the population”. All this is also true, as far as other governmental programs are concerned, since it is impossible to regard as concrete, achievable, realistic, and time-specific such goals as “Guaranteeing the accessibility of medical care and improving the efficiency of medical services, that have to match the sickness rate and the needs of the population, as well as the latest achievements of the medical science, in the amounts, kinds and quality” (governmental program 01 “The development of health care”); “Creating the legal, economic and institutional environment, favourable for the effective development of the labour market” (governmental program 07 “The support of employment of the population”). The examples given vividly demonstrate that a number of the objectives cannot be recognized as “effective”, and, as it is commonly known, ineffective goals can easily “lead in the wrong direction”. You can act efficiently; execute all the claimed operations –but still move in the wrong direction. That is why, to guarantee the achievement of the desired (pre-planned) outcomes, the goals must be really effective ones.

It cannot be denied, that there are serious problems with the logical structure of the programs, most of which lack the sections with the information about the interdependence with the bordering governmental programs. Besides, the controversy on the upper limit of the budgetary appropriations to be approved for their implementation led to ending up with a trade-off decision in 2013, that permitted the formation of all governmental programs in 2 variants/scenarios: a basic scenario (within the approved budget for 3 years) and an additional desirable one, which would allow additional amounts of budgetary appropriations, providing the indicators change in the desirable direction. This led to the approval of the majority of the adopted governmental programs in 2 scenarios (a basic one and an additional one) in the year 2013. Moreover, the approved programs differed in formats, because essential changes had taken place in the regulatory and legislation basis during that time. It caused a substantial restructuring of the actual programs in the middle of the year 2014, however, the new editions of the programs are far from being perfect, either (http://programs.gov.ru).

An important trend in program budgeting is allocating the expenditures to specific purposes and evaluating their effectiveness on the basis of measurable parameters. This system is an especially significant one, providing the fact that evaluating the efficiency of budget expenditures is currently becoming one of the most important tools in the budgetary policy of the nation (Keynes, 1936; Kutivadze, 2012; Modigliani, 1961; Moore & Chrystol, 2008; Siti & Mohd & Podivinsky, 2013). Its role becomes even more relevant under the condition that we want to get a more transparent federal budget and more involvement of the community in the budgetary process.

Furthermore, the problem of taking into account the influence of various factors can be solved within the framework of building a model of an integral system for assessing the efficiency of governmental programs, a part of which would be assessing the efficiency of budgetary expenditures (Sutherland & Hoeller, 2012; Schclarek, 2005).

The task of designing an integral system of budget expenditures remains one of the most urgent (Shush, 2011; Shush & Afanasiev, 2013). It is partly connected with the period of financial instability and the distinct trend to the disproportional amount of expenditure obligations of the Russian state, while the overall budget revenues are decreasing. In such a difficult situation in the sphere of public finance, developing an effective system of assessing the efficiency within the frames of the implemented governmental programs will allow revealing the most and the least productive trends in government expenditures, and also, creating a real basis for boosting their effect (Shush & Afanasiev, 2014).

According to the authors, a governmental program/subprogram can be regarded as a set of economic interactions for achieving various kinds of effects (social, economic), which presumes employing the following principles of assessment (Figure 2).

The Principle The Description

|

Table 3 |

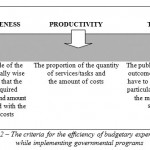

It is especially vital to estimate all governmental programs from the point of view of the efficiency of budget expenditures. Traditionally, the following criteria are applied for assessment

|

Figure 2: The criteria for the efficiency of budgetary expenditures, while implementing governmental programs |

The above given criteria are closely interrelated and indicate different dimensions of the efficiency of social expenditures throughout the process of developing and executing the program budget.

The assessment and comparing the expenditures with the outcomes are unavoidable for preparing justified solutions that concern the appropriateness of the programs’ implementation. The following parameters should be defined: a) the components of the expenditures, b) the economic indexes that allow estimating various elements of the expenses and of the results on the same scale, c) the net return (the difference between the outcomes and the expenditures, including the difference between the public benefits and the public expenditures).

The criteria for assessing the impact reflect only the comparison between the results obtained by means of this amount of expenditures and the planned figures at the stage of the program’s approval. This group of the criteria demonstrates the degree to which the goal was achieved, and the extent to which the tasks were solved for a selected direction of budget expenditures. Meanwhile, the impact criteria might not reflect to which extent the implementation of program operations adhered to the established administrative procedures required while carrying out the expenditures, neither consider the efficiency with which it was managed to obtain the goal’s achievement or the solution to the program’s tasks. The impact can be achieved regardless of the constantly growing budget expenses, that is, to have a “scale effect”, as well as without improvement in the quality of the public services – or, sometimes, even if the quality deteriorates.

When evaluating governmental programs, special attention should be paid to calculating the indicators of not mere economical efficiency, but of social efficiency as well.

The indicators of social efficiency reflect financial and industrial results from the implementation of the governmental programs, they signify certain economic benefits, equally for the consumers of the government services (organizations and individuals) and for the government agencies that implement those programs. Particularly, the economical effect from the implementation of ecological programs can be measured by the increase in the retained total cost of natural resources in the territory of their enforcement.

The indicators of social efficiency take into account the social-demographic consequences from implementing the steps of the environmental program for the society as a whole; the degree of their usefulness that is characterized by the better health of the community, a decrease in the number of diseases and deaths due to the reduction of harmful substances emissions into the environment.

The question of the choice of the indicators, that are to be included into the systems of efficiency measurements, is, in essence, the question of receiving the feedback for further improvement of governmental programs (Shush, 2011; Shush & Afanasiev, 2013). Apart from the control functions, the important moment that should draw our attention is that the figure/indicator, in fact, informs us what is happening (such as quality, cost, etc.). One must understand why this is happening or – does not happen, and this information is to be given by the indicators of efficiency and by nothing else – that are the measurement of the degree in the achievement of the planned results, using a certain amount of resources. Another problem in estimating the efficiency is that the methodologies suggested in the governmental programs do not have the option of estimating the levels of the indicators depending on the amounts of financing (along with the option of multi-variant calculation for the indicators of efficiency and for the forms of getting the data reports).

The specifics of the objectives, tasks, operations and results of some governmental programs is in the fact that the effects achieved because of their implementation are indirect, mediated and deal with not only the promotion in the spheres of their realization, but also with the level and quality of life of the community, with the development of the social sphere, economy, social security, government agencies and so on. All this does not allow adequately measuring the efficiency of the implemented governmental programs. Besides, when evaluating many of the governmental programs of the Russian Federation, special attention should be paid to calculating not only indicators of economical efficiency, but also the social ones. If we turn to the Russian practices, we will see that this is especially vital for social programs from the block “The new quality of life”, such as “The assistance to the community with the employment”, “The promotion of health care”, “The progress in education”, “The development of the pension system” and others.

Let’s see what the specifics of various groups of indicators mean, taking as an example the implementation of some subprograms included into the governmental program “Protecting the environment” for the years 2012-2020 (the block “The new quality of life”), with the amount of expenditures for the year 2014 – 31.7 billion roubles, which aims at improving the environmental safety and preserving natural biological systems.

When developing and implementing the subprograms with ecological aims (“Regulating the quality of the environment”, “The biological diversity of Russia”, “Hydrometeorology and monitoring the environment”), it is important that the costs should be aimed at achieving specific goals, and their efficiency be estimated on the basis of measurable indicators. This requires factoring in a complex of indicators, that allow assessing the ecological efficiency as well as the social and economic efficiency (Shush & Borodin, 2014).

The examples of indicators for the ecologically aimed programs are given in Table 4.

Table 4: The examples of indicators for assessing the efficiency of ecologically-aimed programs*

|

THE INDICATORS FOR THE SYSTEM OF MEASURING THE EFFICIENCY OF ECOLOGICAL PROGRAMS |

|

|

The indicators, factoring in the ecological effect |

The amount of solid wastes produced per person[1] |

| % of produced industrial wastes | |

| % utilized industrial wastes | |

| % of produced consumption wastes | |

| % of utilized consumption wastes | |

| % of factories that have improved the indicator of emissions of harmful substances | |

|

The indicators, factoring in the social effect |

% of sickness rate caused by the pollution of the environment |

| % of deaths, caused by the pollution of the environment | |

| The social effect from the investment into protecting the environment. | |

|

The indicators, factoring in the economical effect

|

The resource consumption level in the economy |

| The energy consumption indicator of the production | |

| The relative proportion of green-labelled products | |

| The economical effect from the investment aimed at the protection of the environment. | |

| The increase in the value of territories after the environment protection measures | |

| The increase in the amount of sanctions for violating the ecological regulations | |

| The total sum of economical loss from the deterioration of the environment | |

* The source: offered by the authors

[1]This is a very meaningful indicator, since in the RF the average figure of producing solid wastes per person ranges within 0.4 tons. Equally important are the figures of utilizing solid wastes, because, presently, less than 40% of the industrial wastes are reprocessed, and only 7-10% of solid household wastes. At the same time, the annual increase in the amount of solid household wastes is becoming one of the major sources of pollutionThe indicators of ecological efficiency can help to most objectively evaluate the impact of the implemented operations on the condition of the environment, which could manifest itself in changes for the better in the composition of water, air, soil, and in the environment as a whole, to include an increase in the assimilative capability of the territory. It could also be the indicators, that characterize dynamics in the decrease of the amounts of polluting emissions and sewage, as a result of applying highly effective treatment facilities, of introduction of advanced industrial technologies, introducing waste-free technologies, which can produce a significant positive impact on the environment and enlarge its biological diversity, improve the assimilative capability of the territory (Shush & Afanasiev, 2013; Shush & Afanasiev, 2014). Also, it could be the indicators that characterize the dynamics in decreasing harmful emissions and sewage. As a result, the environment becomes less polluted, and, therefore, more resistant to the influences of human economic activity.

The social or ecological efficiency can take forms of limiting or eliminating the negative effect of the economic activity on the society and the environment, as well as reveal itself in a higher level of health of the population and in restoring the natural resources and elements that are vital for providing healthy habitat for humans. The priority here is to be given to the programs that are aimed at preventing the pollution of the environment

It should be highlighted that the evaluation of ecological and social efficiency should be prior to measuring the economical efficiency, because the economical effect from the implementation of the programs is weighted against social and ecological benefits and losses.

The criteria for evaluating the efficiency of budgetary expenditures demonstrate the relationship between the costs and the results from making the expenditures. Meanwhile, the efficiency of the budgetary expenditures reflect the level of the resources that were required to achieve particular results.

When creating an integral system of measurement of the efficiency and effectiveness of the programs, groups of indicators are selected for the criteria, mentioned above, which allow giving quantitative measurement to the program activity of a ministry/agency, while conducting the program’s operations.

Program budgeting presumes creating an elaborated system of program’s monitoring and evaluation, that need a complex of indicators, effective procedures of inside and external control.

At the same time, it should be highlighted that the techniques for measurement can vary, depending on the orientation of the program. For instance, ecological programs are assessed during their implementing, as well as after the list of the programs operations is executed, since the effect from the operations may not be immediate. The assessment has to give the opportunity for uncovering the shortcomings, mistakes that happened at the stages of development and implementation of the programs.

The results of assessment can be used for analyzing the efficiency and effectiveness of the program’s operations. It will provide the opportunity to substantially refine the quality of the development of the programs. If the program was a multi-year program (which is typical for programs in the ecological sphere), the annual estimation of the achieved outcomes will allow modifying the operations in the following years.

Additionally, conducting a thoroughly elaborated procedure of assessment of the efficiency reveals the cause-and-effect relations between the outcomes and the program’s operations. At the same time the in-depth analysis of the outcomes and efficiency of the operations bears not only advantages, it has its disadvantages. The main advantage is in getting the most detailed and reliable information, the disadvantage comes in financial and time expenses.

Thus, we can conclude that aggregated assessment of the efficiency with which the governmental programs are implemented offers an opportunity for an objective, aggregated estimation of the effect from the financial resources invested by the state. Systematic evaluation of the effectiveness of the government’s programs is an important instrument of realization of the national policy in a particular area of the government’s activity. Additionally, judging by the results of such systematic evaluation, there can be suggested steps for making the programs more effective in any area.

Besides, the planning of the budgetary expenditures must not be viewed only as aimed at achieving an optimal distribution of resources among the goals of the government’s activity. Program budgeting presents an opportunity not only to evaluate expenditures for the achievement of some objective, but also to analyze their impact within one program, or even a particular operation, and to measure the achieved results against the expenses.

In other words, the contemporary concept of program budgeting solves the problems of achieving both allocating and economical efficiency of expenditures, that arise due to the non-market essence of the provision of public services.

Results

Specifics of the program budget of the Russian Federation are dealt with, the main problems arising in the course of development and realization of state programs are revealed and the measures directed at increase of their efficiency are suggested. It is proved that the main direction of program budgeting is orientation of expenses at the specific purposes and an assessment of their efficiency on the basis of the measured indicators that demands creation of complete system of an assessment of state programs efficiency that reveals the most and the least effective directions of the public expenditures, and also to create real prerequisites for increase of their efficiency. On the basis of the analysis of the state programs realized now, the criteria of efficiency of the budgetary expenses, such as profitability, productivity, productivity are defined. Groups of the indicators applied in the system of an assessment of state programs efficiency of an ecological orientation are considered and it is revealed that the specifics of the purposes, tasks, actions and results of some state programs such is that and the effects gained as a result of its realization are indirect, mediated and belong not only to development of spheres within which such programs, but also to the level and quality of life of the population, development of the social sphere, economy, public safety, the state institutes are realized. In this regard budgeting program assumes creation of the developed system of monitoring and an assessment of programs which needs a complex of indicators, effective procedures of internal and external control.

Conclusions

The conclusion is drawn that the complex assessment of efficiency of state programs realization gives opportunity of the objective, aggregated effect assessment from the financial resources enclosed by the state. The systematic assessment of state programs efficiency is the important tool for determination of efficiency of a state policy realization in concrete sphere of activity of the government as carrying out carefully worked procedure of an assessment of efficiency reveals relationship of cause and effect between results and program actions. Besides, following the results of such systematic assessment measures for increase of efficiency of programs for all directions can be suggested.

References

- Anderson Ph., Anderson C. S., Velandia-Rubiano A. Public Debt Management in Emerging Market Economies: Has This Time Been Different? / World Bank Policy Research Working Paper. 2010. No. WPS 5399. – 28р.

- Barro R. The Ricardian Approach to Budget Deficits // Journal of Economic Perspectives, 1989, № 2, Р. 37-54.

- Checherita C. and Rother P. The Impact of High and Growing Government Debt on Economic Growth An Empirical Investigation for the Euro Area // European Central Bank WP, 2010, № 1237, P. 1-40.

- Cochrane J. Understanding policy in the great recession: Some unpleasant fiscal arithmetic // European Economic Review, 2011, № 55(1), P. 2-30.

- Gale W., Orszag P. The Economic Effects of Long-term Fiscal Discipline // Urban-Brookings Tax Policy Center Discussion Paper, 2003, № 8, P. 1-30.

- Groneck M. A golden rule of public finance or a fixed deficit regime?: Growth and welfare effects of budget rules // Economic Modelling, 2010, Vol. 27, № 2, P. 523-534.

- Elmendorf D., Mankiw G. Government debt.: Handbook of Macroeconomics, 1999. – 82p.

- Hanson J. The growth in government domestic debt: changing burdens and risks // Policy Research WP Series, 2007, № 4348, P. 1-38.

- Keynes J. The General Theory of Employment, Interest and Money. – L.: Macmillan Cambridge University Press, 1936. – 352p.

- Kutivadze N. Public debt, domestic and external financing, and economic growth // Departmental WP, 2012, № 12, P. 1-35.

- Modigliani F. Long–run implications of alternative fiscal policies and the burden of the national debt // Economic Journal, 1961, № 71, Р. 730-755.

- Moore W., Chrystol T. A meta-analysis of the relationship between debt and growth // Munich Personal RePEc Archive Paper, 2008, № 21474, Р. 1-23.

- Siti N., Mohd D., Podivinsky J. Revisiting the role of external debt in economic growth of developing countries // Journal of Business Economics and Management, 2013 Р. 968-993.

- Sutherland D., Hoeller P. Debt and Macroeconomic Stability: An Overview of the Literature and Some Empirics // OECD Economics Department WP, 2012, № 1006, P.1-35.

- Schclarek A. Debt and economic growth in developing and industrial countries // LundUniversity Working Papers, 2005, № 34, Р. 1-39.

- Shush, N.N., 2011. Designing a program budget and assessing the efficiency of the programs. The scientific research financial institute. The Finance Magazine, 2: 55-64.

- Shush, N.N. and M.P. Afanasiev, 2013. The inventory of assessment the effectiveness of governmental programs. The issues of the state and municipal administration, 3: 58-69.

- Shush, N.N. and M.P. Afanasiev, 2014. Russian budgetary reforms: from the programs of social and economical development to the governmental programs of the Russian Federation. The issues of the state and municipal administration, 2: 48-64.

- Shush, N.N. and M.P. Afanasiev, 2014. The government’s debt obligations in the system of financing the national debt. The science vector of the Tolyatti State University, Series: Economics and management, 2(17): 58-61.

- Shush, N.N., A.I. Borodin and A.A. Tatuev, 2014. Vectors in budgetary centralization and the efficiency of budget regulation. Finances and Credit, 35(611): 2-10.

- Shush, N.N. and A.I. Borodin, 2014. The priorities in the budgetary policy of Russia and the regional budget problems. The Herald of the University of Udmurtia. Series 2: Law and Economics, 1: 116-123.

This work is licensed under a Creative Commons Attribution 4.0 International License.